:max_bytes(150000):strip_icc()/100877758_finance_marketing-c3a83596b1e74508a80a72db8b9e4b60.jpg "New Program Helps Farmers Apply for USDA Grants")

:max_bytes(150000):strip_icc()/Lifsey-HeleneMud-3f398e7abf854100b053e20d361f29d2.jpg "One USDA Staffer Is Handling All of Western NC’s Post-Helene Farm Loans After Federal Cuts, Freeze")

:max_bytes(150000):strip_icc()/kathyholt5.12-scaled-e1747109716219-2048x1403-bb745c9246b6446fbdf98ce4b6ccd41e.jpg "Iowa Senate Passes Bill Restricting Eminent Domain for Carbon Pipelines")

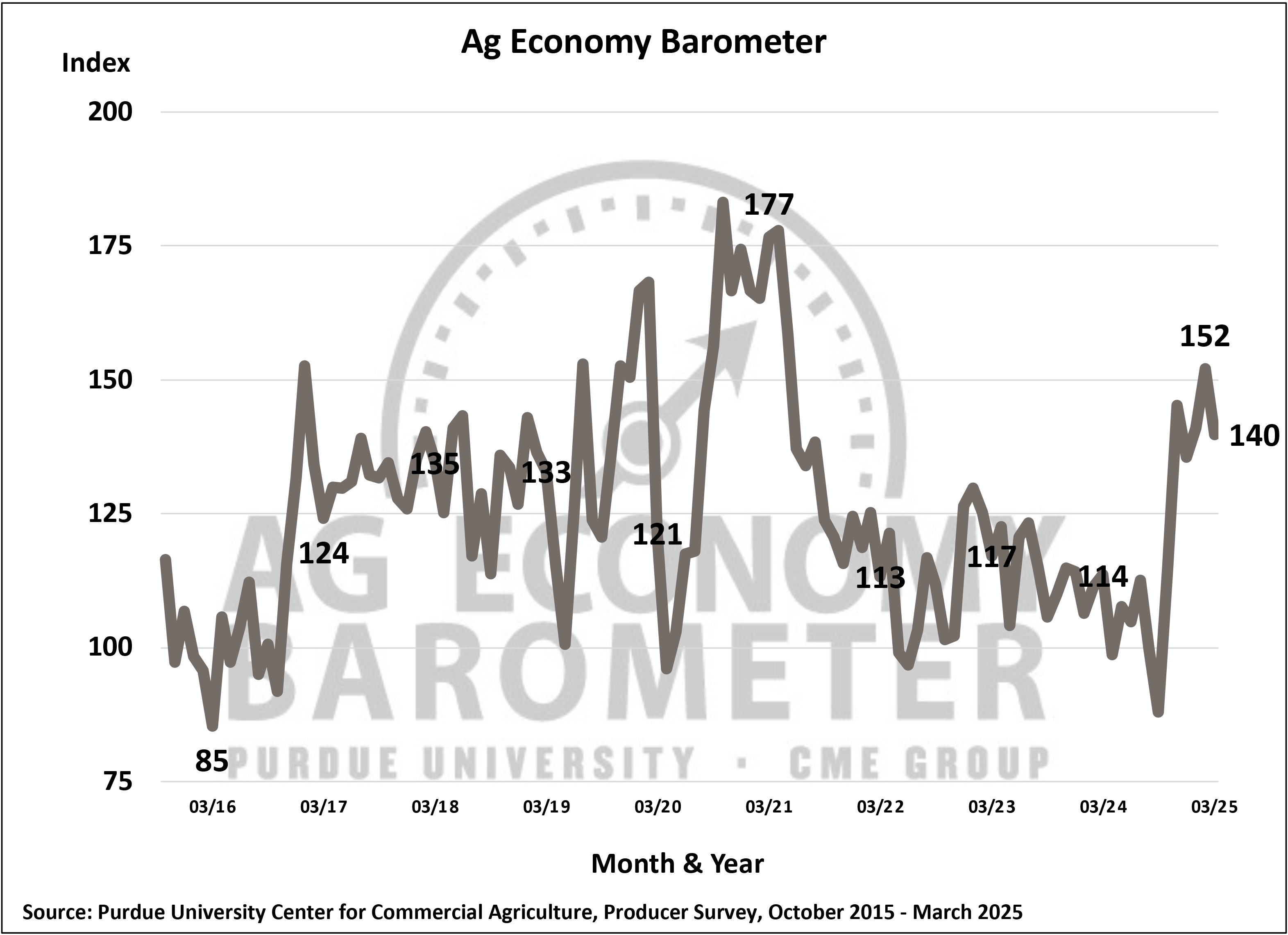

Farmer sentiment declined in March as concerns over agricultural trade and farm policy weighed on producers’ outlook for the future. The Purdue University/CME Group Ag Economy Barometer fell 12 points to a reading of 140, down from 152 a month earlier. Contributing to the weakened sentiment in March was a 15-point drop in the Index of Future Expectations to 144 and the Current Conditions Index falling 5 points to 132.

This month’s survey was conducted between March 10 and 14.

The drop in sentiment was influenced by falling crop prices since mid-February, along with increasing uncertainty surrounding agricultural trade and farm policy. Despite the decline, producers remained more optimistic about future conditions than the present, with the Future Expectations Index remaining higher than the Current Conditions Index by 12 points.

Alongside the weakened sentiment, the Farm Capital Investment Index fell 5 points to 54 in March. Despite the dip, it is the second-highest reading since June 2021. The Farm Financial Performance Index also saw a drop, decreasing 8 points to 102. While slightly above 100, the index indicates that, on average, producers still anticipate their farm’s financial performance to improve compared to a year ago.

Farmland values hold steady despite declining sentiment

The Short-Term Farmland Value Expectations Index remained steady at 118 in March, matching the previous month’s level and only 6 points below its reading from a year ago. Except for the late summer and early fall of 2024, when sentiment was more pessimistic, the index has generally ranged between 110 and 126 since early 2023. This suggests that farmers maintain a cautious outlook for farmland values, anticipating they will either remain stable or increase modestly in the coming year.

While the overall sentiment shift in March reflects growing uncertainty, farmers remain cautiously optimistic about the future, particularly with farmland values holding steady and the outlook for strong returns in the livestock sector helping to offset weaker expectations among crop producers.

Expectations for agricultural exports hit record low

Since 2019, the barometer surveys have asked producers about their expectations for U.S. agricultural exports over the next five years. Historically, exports have been a primary driver of U.S. agricultural production demand and are closely linked to strong farm incomes. Producers reported they were optimistic about export growth in 2019 and 2020 surveys, but that optimism began to decline in 2021 and has continued to erode.

In March, expectations for U.S. exports reached a record low in the survey, with 30 percent of producers anticipating a decline in exports, nearly matching the 33 percent who expect exports to rise.

In addition to worries about exports, farmers’ focus on agricultural policy has shifted over the past year. Since late 2022, barometer surveys have regularly asked producers to identify the most important policies or programs for their farms in the next five years. Before the November 2024 election, farmers reported a higher focus on interest rate policy than trade policy.

However, since the election, trade policy has become a fast-growing concern, with 43 percent of respondents, on average, now citing it as the most critical issue impacting their farms, up sharply from an average of just 21 percent prior to the election.

Uncertainties about trade policy and its potential impact on U.S. agricultural exports are closely tied to farmers’ expectations for farm income. The March survey asked producers about the likelihood of a program similar to 2019’s Market Facilitation Program, created to compensate for lower output prices due to a trade war.

Approximately two-thirds of respondents believe a follow-up to such a program is either “likely” (52 percent) or “very likely” (13 percent) to be implemented. Additionally, 74 percent of farmers in March indicated that the passage of a new farm bill this year was either “very important” (49 percent) or “important” (25 percent) to them.

:max_bytes(150000):strip_icc()/IMG_8587-2048x1365-d8523fae626b46f683a5be829dab042c.jpg "Iowa Lawmakers Approve Budget for Agriculture, Natural Resources")

:max_bytes(150000):strip_icc()/KernDronePatternFlightWEB-a12123c08e734ea0ada3ff441c2bb6fc.jpg "Maximizing Farm Efficiency With Drones")

:max_bytes(150000):strip_icc()/IMG_9383edit-2048x1339-f6bb0401ee7940b38f528be3cd725cfa.jpg "2 Lawsuits Against Summit Allowed to Advance; A Third Case Is Pending")