International Development

ISSN 1470-2320

Prizewinning Dissertation 2021

No.21-CC

International Remittances and the COVID-19

Pandemic: Investigating Resilient Remittance

Flows from Italy during 2020

Carla Curreli

Published: Feb 2022

Department of International Development

London School of Economics and Political Science

Houghton Street Tel: +44 (020) 7955 7425/6252

London Fax: +44 (020) 7955-6844

WC2A 2AE UK Email: d.daley@lse.ac.uk

Website: http://www.lse.ac.uk/internationalDevelopment/home.aspx

DV410 23759

Abstract

Defying the predictions of the World Bank, international remittances flows have proven resilient amid the COVID-19 pandemic. Recent literature has pinpointed several factors that help explain this pattern. Focusing on Italy as a case study, this work relies on semi-structured in-depth interviews to investigate migrants’ experiences with sending steady flows home during 2020. It finds that respondents faced a higher demand for remittances from their families abroad due to COVID-19, while their ability to send money was constrained by employment disruption and insufficient emergency support. To sustain stable fluxes, migrants turned to coping strategies including reduced consumption, reliance on savings and social networks, as well as a combination of formal and informal remittance channels.

DV410 23759

Table of Contents

Abstract ……………………………………………………………………………………………………………………..

List of Abbreviations …………………………………………………………………………………………………..

List of Figures and Tables…………………………………………………………………………………………….

Acknowledgments……………………………………………………………………………………………………….

1. Introduction …………………………………………………………………………………………………………

2. Literature Review ……………………………………………………………………………………………….

2.1 Resilient remittances during 2020: setting and evidence ……………………………………

2.2 Remittances during crises: macro-level and micro-level factors …………………………

2.3 The determinants of steady remittance flows in 2020………………………………………..

3. Case Study Selection: Italy …………………………………………………………………………………..

3.1 Migration and Remittances Trends in Italy ………………………………………………………

3.2 Government support, migrant employment and RSPs accessibility …………………….

3.3 The Province of Pistoia …………………………………………………………………………………

4. Methodology ………………………………………………………………………………………………………

5. Findings …………………………………………………………………………………………………………….

5.1 A commitment to the family: higher demand for remittances …………………………….

5.2 Sustaining remittance supply …………………………………………………………………………

5.2.1 Migrants’ employment status and government support ……………………………………

5.2.2 Coping strategies: savings and reduced consumption ………………………………………

5.2.3 Coping strategies: reliance on social networks ………………………………………………..

5.3 Remittances channels ……………………………………………………………………………………

5.4 Discussion …………………………………………………………………………………………………..

6. Conclusion …………………………………………………………………………………………………………

Bibliography …………………………………………………………………………………………………………….

DV410 23759

List of Abbreviations

CIG Redundancy Fund

OECD Organization for Economic Cooperation and Development

IMF International Monetary Fund

LMICs Low- and Middle-Income Countries

MTO Money Transfer Operator

REM Emergency Income

RSP Remittance Service Providers

UN United Nations

WB World Bank

List of Figures and Tables

Figure 1 – Remittance Flows and Yearly Percentage Change in Remittance Inflows towards

LMICs.

Table 1 – Remittance Inflows by Year and Region.

Figure 2 – Foreign Population Resident in European Countries.

Figure 3 – Quarterly GDP at Constant Prices, Comparison Between European Countries.

Table 2 – Remittances from Italy; Foreign Resident Population; GDP; Unemployment Rate.

Table 3 – Remittance Outflows from the Province of Pistoia (Tuscany).

DV410 23759

Acknowledgments

I would like to express my gratitude to the migrants who eagerly shared their time and stories building this study. Meeting them was an enriching human and research experience.

DV410 23759

1. Introduction

International remittances play a role of utmost importance in the global development agenda. Defined as financial or in-kind transfers made by migrants to relatives and friends in their country of origin, remittances represent a lifeline for many families (Ratha, 2017). Research on the micro-level impact of remittances has shown that, in the presence of poorly functioning credit markets, remittances represent a form of informal insurance against several types of shocks (Lucas & Stark, 1985; Rapoport & Docquier, 2006), including income and health shocks (Gubert, 2002; Beuermann et al., 2016). Other scholars highlight the role of remittances in strengthening local human development through investments in health and education (Yang, 2008; Gyimah-Brempong & Asiedu, 2015), as well as capital investment (Woodruff & Zanteno, 2007).

Based on this evidence, the UN Sustainable Development Agenda conceptualises international remittances as a means to reduce inequality between countries, and the Sustainable Development Goal 10.c urges governments to reduce the transaction costs of migrant remittances to foster global fluxes (UN General Assembly, 2015). Given the importance of remittance flows as economic lifeline and insurance tools, it is expected that sudden stops in migration and remittance streams will increase poverty and reduce household access to primary services. In April 2020, the World Bank (WB) released worrisome predictions on the impact of the COVID-19 pandemic on remittance flows to low- and middle-income countries (LMICs) (Ratha et al., 2020). Remittances were projected to decrease by 19.7 percent due to the economic crisis which negatively affected wages and employment for migrant workers. However, these predictions have recently been proven wrong. In May 2021, updated figures showed that remittances flow to LMICs fell by only 1.6percent , defying the claim that COVID-19 would have triggered the sharpest decline in recent history (Ratha et al., 2021).

Recent works published between 2020 and 2021 delved into the study of stable remittances by pinpointing some factors contributing to resilient flows, including fiscal stimuli propping up economic activity in main sending countries (Ratha et al., 2021) or shifts from informal remittance channels to formal ones (Dinarte et al., 2021). However, this literature has exclusively undertaken a quantitative approach to the topic, relying on quantitative analysis to describe relationships between resilient remittances and macroeconomic factors in the major sending economies (WB, 2021a; Dinarte et al., 2021) or survey data analysis (RCTF, 2020; Orozco & Klaas, 2021). Thus, research has foregone to study the personal experiences of migrants’ steadily sending money home amid the COVID-19 pandemic, including the motivations to ensure stable fluxes, their related challenges and coping strategies. The present study seeks to fill this gap with a regard to the context of Italy in 2020.

DV410 23759

Italy represents an interesting setting to study remittance resilience, given its migration and remittances trajectories, and economic outlook during the pandemic. Italy hosts the fifth largest population of foreign citizenship in Europe (Eurostat, 2021), and ranks among the largest host countries in terms of immigrant stocks (UN DESA, 2019). Although its economy was deeply hit by the crisis generated by COVID-19 and no relevant increase in regular foreigners was recorded (ISMU, 2021), remittance outflows from Italy in 2020 have proven much resilient than other countries with comparatively large migrant populations, recording a net increase between 2019 and 2020 and a positive increase in every quarter (Bank of Italy, 2021). Using a qualitative methodology, this study conducts semi-structured in-depth interviews with a sample of 21 migrants working and living in the Province of Pistoia (Tuscany) to shed light on why remittance flows remained resilient during 2020, and how migrants experienced and could sustain greater fluxes.

The results show that most of migrants interviewed sent stable or higher remittance flows during 2020. To explain this, respondents mentioned a greater demand for economic support coming from their families abroad. Greater demand was due to a deterioration of the economic conditions of the migrants’ countries of origin – including inflation and the disruption of economic activities due to local lockdowns – as well as the need of supporting family members directly affected by the COVID-19 economic and health crisis. Once faced with greater demand from their families, migrants’ ability to remit was conditional on their employment status and constrained by scarce government support. Thus, they sustained steady remittances by implementing a set of coping strategies, including reduced consumption, reliance on savings, seeking support from social networks, and reliance on a combination of formal and informal channels. Overall, the present study claims that an analysis of resilient remittances in 2020 must factor in the variables shaping the demand for remittances as well as their supply, with a focus on the personal experience of remittance receivers and senders and the factors hindering migrants’ ability to remit.

The work is structured as follows. Section 2 discusses the case of resilient remittance flows during 2020, before theorising the determinants of remittances in times of crises and reviewing recent literature seeking to explain remittances trends in 2020. Section 3 introduces background information on the Italian case study, examining the Province of Pistoia where the analysis took placeSection 4 describes the methodology. Section 5 presents the findings of the interview and discusses them in light of the theoretical contributions. Section 6 concludes.

DV410 23759

2. Literature Review

2.1 Resilient remittances during 2020: setting and evidence

In April 2020, the WB provided a first estimation of the impact of COVID-19 on international remittance flows. Based on data from the Balance of Payment statistics of the International Monetary Fund (IMF), Ratha et al. (2020) estimated a decline of remittance flows to LMICs from $554 billion in 2019 to $445 billion in 2020, representing a reduction of 19.7 percent Three main reasons were initially flagged to justify this trend. First, the decline was believed to result from a drop in earnings and employment levels of migrant and foreign workers in host countries as a result of COVID-19, rather than a decrease in the stock of international migrants (Capps et al., 2020; Sanchez et al., 2020).

This hypothesis aligns with estimates of OECD (2020a), recording a fall in foreign-born employment for major migrant destinations such as the United States and Germany, as well as oil-dependent sending economies affected by a drop in oil price (OECD, 2020b; IMF, 2020a). Second, national lockdowns and social distancing measures were likely to limit physical access to brick-and-mortar remittance services providers (RSPs), increasing the barriers to international transactions (Benni, 2021). Finally, preliminary evidence showed that several countries did not offer financial support to economic migrants, constituting a major group of remittance senders (Ratha et al., 2020).

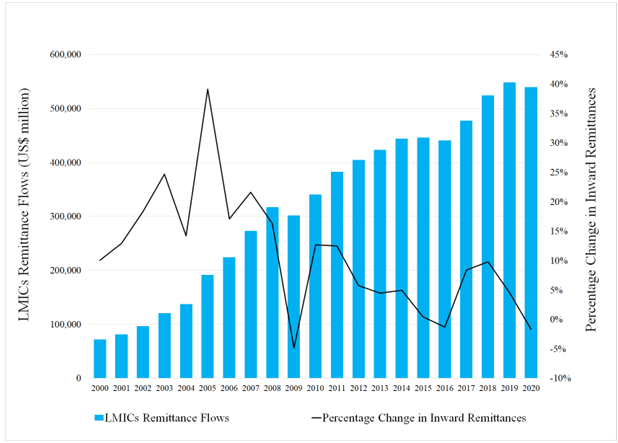

Although estimates have been revised through 2020, remittance flows proved extremely resilient in contrast to WB’s initial forecasts. A novel dataset published in May 2021 by the WB (2021b) showed that officially recorded remittance flows to LMICs fell of only $8 billion between 2019 and 2020 (Ratha et al., 2021). As shown in Figure 1, this corresponds to a reduction of -1.6%, considerably lower than the drop of nearly 5% registered as a consequence of the Global Financial Crisis between 2008 and 2009 (WB, 2021b). Moreover, remittance flows proved more supple than foreign direct investment (FDI) flows to LMICs, which declined by 11 percent in 2020 (Ratha et al., 2021).

Figure 1 – Remittance Flows and Yearly Percentage Change in Remittance Inflows towards LMICs. Own elaboration based on WB (2021b).

DV410 23759

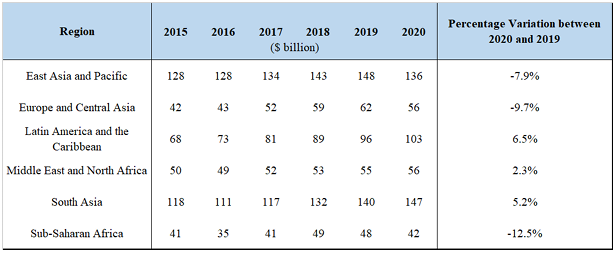

By disaggregating the data at the regional level, interesting between-region variations can be highlighted. Remittance inflows rose in Latin America and the Caribbean (6.5%), South Asia (5.2%), Middle East and North Africa (2.3%).Conversely, remittances towards Sub-Saharan Africa fell by 12.5 percentage points. A fall in remittances was also observed in East Asia and the Pacific (-7.95) and Europe and Central Asia (-9.7%). Such variation is expected to mirror great heterogeneity in the pandemic’s impact on migrants’ countries of origin, and differences in preferred migration destinations.

Table 1 – Remittance Inflows by Year and Region. Own elaboration based on WB (2021b).

DV410 23759

2.2 Remittances during crises: macro-level and micro-level factors

Resilient remittances in 2020 can be discussed in light of existing theories on how remittance flows respond to localised or diffused shocks, as well as the macro and micro-level determinants influencing them. First, there is a broad agreement within the literature that remittances are countercyclical with regard to downturns and crises in migrants’ countries of origin. Frankel (2011) undertakes a global study of bilateral remittances flows, showing that remittances respond positively to the cyclical position in the sending country (the migrant’s host) and negatively to the cyclical position in the receiving country (the migrant’s place of origin).

This pattern is further highlighted by Gupta (2006), illustrating that remittances inflows to India are higher when the country undergoes periods of lower economic growth. However, estimations of countercyclicality presume that migrant labour conditions abroad are unrelated to consumption shortages, or lower growth, in countries of origin (WB, 2021a). Yet, COVID 19 is a global shock, hitting the economy of remittance-recipient countries as well as remittance senders. In this regard, literature on the Global Financial Crisis provides evidence of the effects of crisis affecting sending countries on remittances (Sirkeci et al., 2012). Countries depending on remittances from the United States, such as Latin American countries, experienced declining remittances following the impact of the Global Financial Crisis on the US labour market (Ruiz & Vargas-Silva, 2009; Sidaoui et al, 2010; Acosta et al., 2012). Similar evidence is collected for African countries whose migrants mostly resided in Europe, reporting significant remittance declines due to employment falls in hosting countries (Barajas et al., 2010), and South Asia (Raihan, 2010).Hence , remittance flows in 2020 are expected to depend on the economic outlook of both sending and receiving countries.

DV410 23759

As countercyclicality only partly accounts for the complex nature of remittances during crises, a discussion on the micro-level determinants of remittances is required. Following Rapoport and Docquier (2006), remittances are generally driven by altruistic motivations, indicating migrants’ concern over the income and consumption levels of those left behind, including their wives, children, parents and members of wider familial and social circles. In this regard, Stark (2009) shows that altruistic migrants base their remitting decision on the income of their family members. This implies that the amount sent by migrants will increase when receiving households experience a situation of greater financial hardship caused by a negative income shock (Chami et al., 2005), and surges in remittances are thus justified through the combination of altruistic and insurance rationales (Tullao & Cabuay; 2016). Empirical evidence confirming the insurance hypothesis is provided by Yang and Choi (2007), claiming that reductions in income caused by exogenous shocks lead to an increase in remittance flows from overseas migrants. Indeed, altruistic and insurance motives might have led migrants hit by the COVID 19 pandemic to sustain remittance flows towards the countries or families hit hardest by the pandemic (Dinarte et al., 2021).Moreover , altruistic rationales can coexist with investment motives: migrants earnings can be spent to make investments in the country of origin that would otherwise be impossible to make, given the credit constraints and high up-front expenditures.

These investments are correlated with higher expenditure on health, housing, entrepreneurial investment, housing (Yang, 2008; Adams & Cuecuecha, 2013; Cox & Ureta, 2003; Hanson & Woodruff; 2003; Osili, 2004). Investment motives might continue to play a role amid the COVID-19 pandemic, especially requiring greater health investments.

2.3 The determinants of steady remittance flows in 2020

As the pandemic unfolds in 2021, research studying steady remittances flows during 2020 is scant. However, there is a nascent strand of literature consisting of theoretical and empirical works setting the basis for further analysis.

Ratha et al. (2021) provide an overview of several drivers that might explain steady remittances flows in 2020. Among the others, the authors claim that the implementation of fiscal stimuli resulted in better-than-expected economic conditions in the main remittance-sending countries, allowing for steady remittances. This statement is justified through quantitative analysis: the authors show that the economic performance of major migrant-hosting countries in North America and Europe was much stronger than forecasted, and was accompanied by a progressive rise in the employment levels of foreign-born. This was due to multi-year fiscal

actions to support households and firms (IMF, 2021b), through which high-income OECD countries mobilised twice as much funding after six months of crisis as they did during the Global Financial Crisis of 2008 (UNCTAD, 2020). Such countercyclical policies softened employment and income falls within migrant and foreign-born persons, and correlate with steady flows. One relevant example in this sense is the CARES Act, implemented in the United States hosting the largest migrant stock worldwide and recording the largest remittance outflows in 2020 (WB, 2021c). CARES Act provided American households with economic impact payments for which green card holders and immigrants with regular Social Security numbers were all eligible (Holtzblatt & Karpman, 2020).

DV410 23759

A second factor explaining steady remittances is linked to the emergence of informal unrecorded flows. While a significant share of remittances traditionally travels through systems linked to the movements of people and goods across borders, lockdowns and quarantines disrupted these channels and poured remittance flows into formal transfer modes (Frigeri, 2020a). Unrecorded flows are shown to depend on the cost to travel, which is heavily driven by distance (Ferriani & Oddo, 2019). As a result, the above explanation better applies to migrants sending remittances to neighbouring countries. The research of Dinarte et al. (2021) on the determinants of rising formal remittances from the United States to Mexico in 2020 confirms this assumption. Through the implementation of a difference-in-difference strategy, the author finds that rising inflows were larger among Mexican municipalities that were previously more dependent on informal channels, i.e. the ones closer to the US border.

Conversely, the authors rule out the alternative hypothesis that fiscal stimuli in the American economy benefitted Mexican migrants and helped explain higher remittances. These findings align with other evidence of geographic mobility and distance as important variables that affect the level of remittances (Frankel, 2011; Docquier et al., 2012; Lueth and Ruiz-Arranz, 2008). Importantly, this claim holds crucial implications for the interpretation of steady flows in 2020. If this channel holds, WB-recorded outflows should not be considered proof of resilient flows, but rather indicate a partial substitution between different channels which might hide a drop in the real amount received by households in the countries of origin.

Increased reliance on formal transfers is partly verified by an uptick in volume and frequency of transactions through digital Money Transfer Operators (MTOs) (Balch, 2020), i.e. financial companies engaged in cross border transfer of funds, including Western Union, Moneygram, and RIA, as well as a 65% increase in international remittances sent and received through mobile money (GSMA, 2021). However, digital platforms process a still small number of transactions, constituting 30% of the total remittance market in 2019 (Benni, 2020). The majority of transactions still entail cash payments happening through RSPs, where the migrants can rely on the mediating support of agents. Thus, resilient remittance flows also depend on the accessibility of RSPs during COVID-19 related lockdowns, depending on whether they were declared “essential” services (RCTF, 2020).

DV410 23759

Coherently with the countercyclical role of remittances, variation in inflows during the pandemic is expected to highly depend on economic variables in migrants’ home and host countries. For example, weak oil prices led to declining outward remittances from oil producing countries such as Russia (WB, 2021c) and the Gulf Cooperation Council countries (Ratha et al., 2021). Similarly, the WB (2021a) conducts a regression analysis to disentangle the main factors leading to higher remittances flows to a subset of LMICs in 2020, and find that appreciation of exchange rates and interest-rate differentials are the most significant explanatory variable.

Finally, some survey-level evidence has been collected to study migrants’ experience with sending remittances during 2020 and 2021. According to an IFAD survey of African diasporas in Europe and North America done in May 2020, the majority of the migrants had to either reduce or suspend remittances (RCTF, 2020). Moreover, most migrants had to cut back on their consumption to continue sending remittances back home. Another survey, conducted on US immigrants from eight Latin American and Caribbean nationalities, finds again that the majority of respondents sent less in 2020 vis-à-vis 2019 (Orozco & Klaas, 2021). Based on the survey, the authors conclude that having higher savings, being “essential workers” (broadly defined as those working in health services, construction, and agriculture), and having children in their country of origin were the strongest predictors of higher remitted amount.

Moreover, the findings show that those sending more in 2020 vis-à-vis 2019 were not financially affected by the pandemic. In line with the predictions of Ratha et al. (2021), both surveys found that migrants relied more on bank transfers, mobile applications, and web portals. In summary, resilient remittances during 2020 are ascribed to multifaceted factors that are context-specific and individual-specific. Thus, they might hold for some individuals living in certain countries, while mistakenly depict the experience of others. In an attempt to narrow down the analysis, this dissertation looks at the context of remittance outflows from Italy.

DV410 23759

3. Case Study Selection: Italy

3.1 Migration and Remittances Trends in Italy

Italy is a particularly relevant case study for analysing resilient outward remittance flows in 2020, for three key reasons.

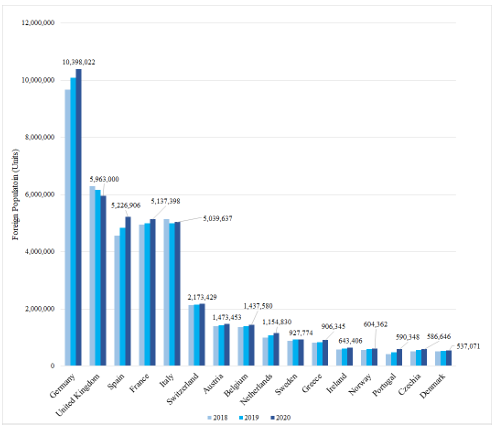

Firstly, Italy hosts the fifth-largest foreign population among the European countries, defined by the OECD (2021a) as the persons born abroad maintaining the nationality of their country of origin. As of 2021, Italy hosts 5 million residents of foreign origin, following Germany (10,4 million), the UK (6 million), Spain (5,2 million), and France (5,1 million) (Eurostat, 2021).

While providing an overall good estimation of migrant presences and being suited for comparison (OECD, 2021a), this indicator imperfectly captures the dynamics of migration flows for leaving aside regular non-resident foreigners and undocumented presences. In 2020, regular non-residents equalled 366,000people , while undocumented presences accounted for 517,000, bringing the total number of foreigners living in Italy to an estimate of 5,923 million (ISMU, 2021).

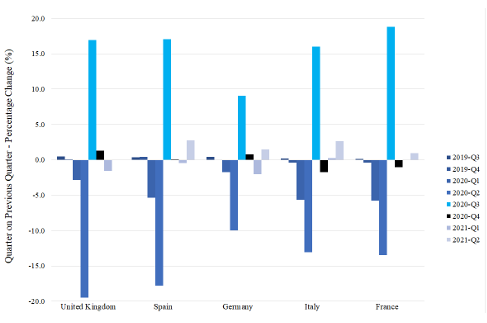

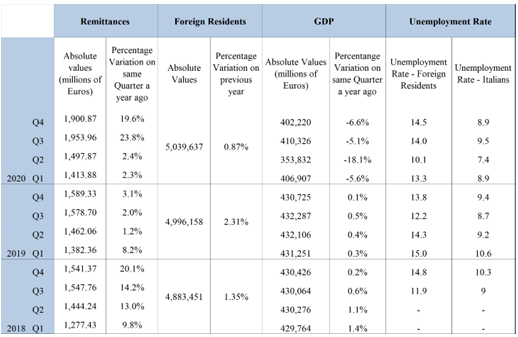

Second, Italy’s economic structure was deeply hit by COVID-19 once compared with other European countries. Quarterly variation of real GDP showed in Figure 3 illustrate the progressive deterioration in Italy’s economic outlook in 2020 compared to 2019. Remarkably, GDP fell by -5.7% between Q1 of 2020 and Q4 of 2019 and by -13% between Q2 2020 and Q1 2020. Despite a partial economic recovery in Q3 (with an increase of 16% vis-à-vis Q2 2020), the GDP contracted by -1.75% in Q4.

The performance of Italy’s economy in 2020 reflect the alternation of total and partial lockdowns enforced in the country during the year . Similarly to the trend observed in the other major European economies, the fall of the GDP in Q2 is attributable to the imposition of a national lockdown starting from March 9th, followed by the closure of all “non-essential activities“from March 23rd. It implied a fall in GDP by 30% vis-à-vis the previous year in the weeks most intensely affected by the lockdown (Delle Monache et al., 2021).

National lockdown measures were gradually lifted starting from May, leading to the rise in economic activity in Q3. The significant contraction experienced in Q4 is peculiar to the Italian case and in stark contrast with the trends in the United Kingdom, Germany and Spain. It coincided with the enforcement, starting from October, of a peculiar zone system entailing different levels of restriction based on the severity of the epidemic in each Italian region (Conteduca, 2021). The economic downturn affected disproportionally foreigners living in Italy compared with Italian citizens. Table 2 shows the significantly higher unemployment rates faced by foreign residents.

DV410 23759

Figure 2 – Foreign Population Resident in European Countries. Own elaboration based on OECD

(2021a).

DV410 23759

Figure 3 – Quarterly GDP at Constant Prices, Comparison Between European Countries. Own

elaboration based on OECD (2021b).

Third, data published by the Bank of Italy (2021) show an unexpected positive trend in remittance outflows. While aggregated data for the 21 European countries pinpoint a decrease in remittances flows by -4% and -8% in Q1 and Q2 of 2020 vis-à-vis Q1 and Q2 of 2019 (European Migration Network, 2020), remittance outflows from Italy present a positive percentage variation for every quarter of 2020 compared to 2019, despite the deterioration of the Italian economy and an almost unchanged foreigners’ stock. Overall, total remittances sent from Italy equalled 6,7 billion Euros in 2020, representing a 12% increase compared to 6,01 billion in 2019 (Bank of Italy, 2021).

DV410 23759

Table 2 – Remittances from Italy; Foreign Resident Population; GDP; Unemployment Rate. Own

elaboration based on ISTAT (2021a-b-c); Bank of Italy (2021).

3.2 Government support, migrant employment and RSPs accessibility

To better conceptualise the resilience of remittance flows during 2020, it is worth providing an overview of the factors that might have played a role in sustaining international transactions, namely government interventions supporting migrants’ incomes and the accessibility of money transfer services throughout the pandemic. Starting from April 2020, the Italian National Social Security Institute (INPS) has taken measures in support of (i) employees, through a wage guarantee fund (Cassa Integrazione Gaudagni, or CIG); and (ii) self-employed and professionals, through a set of income support bonuses introduced in the “Cura Italia“Decree of March 16th. As per law, these transactions were opened to foreigners as well (OECD, 2020a).

Additionally, the “Cura Italia“Decree halted dismissals for five months starting in March. Concerning family assistance, the government devised an emergency income (Reddito di Emergenza, or REM) benefitting households in economic difficulties depending on the size of the family. With regard to enterprises, three Decree Laws defined additional granted funds paid by the Italian Revenue Agency between June-July and November-December (Venditti & Salvati, 2021).

DV410 23759

In Italy, regular residents and non-residents were entitled to the same measures to guarantee employment and salary support to Italian workers (ISMU, 2021). Moreover, while it is often believed that migrant workers often take up informal and undeclared jobs exacerbating their vulnerability, recent evidence has shown that migrant workers tend to be over-represented in those occupations defined “essential“by the European Commission, including the construction sector, stationary plant and machine operations, personal care, food processing, drivers and mobile plant operations, personal services. Remarkably, while only 31% of native Italians are essential workers, figures rise to 43% for migrant workers of European origin and 40% for Extra-European workers, representing one of the largest gaps among European countries (Fasani & Mazza, 2020). Overall, these findings speak directly to the dependence of the Italian health and social sector on the migrant labour force. For the sake of this research, essential workers are expected to be less economically affected by the pandemic, having the possibility of working during the national and local lockdowns and sending more money home.

Finally, migrants’ direct experiences with accessing money transfer services during national and local lockdowns might have impacted the remittances flows sent. In this regard, it is worth mentioning that RSPs in Italy were classified as “essential“since the beginning of March. Accordingly, there has been relatively little impact on service accessibility, with MTO shops, bank branches and post offices remaining open throughout the first lockdown, as well as tobacconist shops (Frigeri, 2020a).

3.3 The Province of Pistoia

Located in Tuscany, the Province of Pistoia is identified as the core study site of the analysis for a reason of research feasibility discussed in Section 4. Regardless, the Province is well suited for analysis. As of January 1st 2021, the foreign population resident in the Province accounted for 9.9% of the total residents, scoring higher than the average for Italian provinces (8.5%). The distribution of foreigners by country of citizenship reflects the overall ethnic composition at the national level, with a majority of the foreigners coming from European countries, including EU-28 members and Central Eastern Europe. Other relevant minorities come from Northern Africa and West Africa, and South Asia. (ISTAT, 2021). Overall, the Albanian diaspora constitutes the most relevant presence on the territory, accounting for 31.9% of the total foreign residents and 3% of the total population. The second-largest minority is composed of Romanian (22%), followed by Moroccans (8.6%), Chinese (5.6%), Nigerians (4.3%) and Pakistani (3%).

DV410 23759

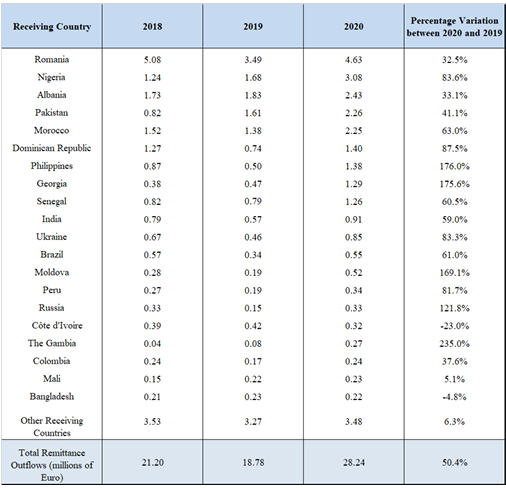

Remarkably, foreign communities in the Province of Pistoia proved to be extremely resilient in sending money home during 2020. Compared to the national 12% increase between 2020 and 2019 previously mentioned, remittance flows from the Province of Pistoia increased by 50% during the same period. Table 3, sorting remittances outflows by quantity and receiving country, shows that Romania and Nigeria were the countries receiving the greatest amounts in 2020, followed by Albania and Pakistan. The percentage variation between 2020 and 2019 was positive for the great majority of the groups indicated.

Table 3 – Remittance Outflows from the Province of Pistoia. Own elaboration based on Bank

of Italy (2021).

DV410 23759

4. Methodology

As shown in the Literature Review section, recent investigations on resilient remittances during 2020 have relied mostly on quantitative methodology, including regression analysis and survey analysis. While this approach is helpful to pinpoint relationships between different macro-level and micro-level variables shaping remittance flows, it fails to capture the experiences of migrants sending money home during the COVID-19 crisis, and the strategies implemented to cope with it. Instead, this dissertation utilises qualitative methodology to explore migrants’ lived experiences within the Italian context. Moving from migrants’ perspectives backward to the factors that allowed for stable flows, this work delves into the causes of effects (Mahoney & Goertz, 2006).

The data collection took place between July and August 2021. It entailed conducting in-depth, semi-structured interviews with a comprehensive sample of foreign workers with legal status to live and work in Italy, including European and Extra-European respondents from 6 countries of origin. The interviewees live and work in the Province of Pistoia (Tuscany), which was chosen for a reason of feasibility, as it constitutes my Province of Residence. Interviews were held in-person (except one, held by telephone) taking the precautionary measures required by the ongoing pandemic, namely wearing masks in closed spaces and keeping social distancing in outside venues. The discussions were conducted in Italian or English, depending on the preferences of the interviewees.

The ’interviewees’ selection process relied on a combination of purposive and “snowball“sampling. First, respondents were selected based on their relevance for the matter researched (Mason, 2002). To provide an informative contribution, having experience with sending remittances before and after the COVID-19 outbreak and being present in Italy during 2020 were set as key inclusion criteria. This allowed the respondents to assess how their experiences changed over time due to the pandemic. Second, the research excluded vulnerable categories with unclear status, as they constitute a hard-to-reach group that might potentially rely on illegal or unauthorised means to send remittances, which are outside the scope of this study. Third, variation in the employment sector and status at the time of the pandemic was encouraged, so to gather informative insights on the sector-differentiated impact of the COVID-19 economic crisis.

DV410 23759

Given the limited time frame to conduct the research, I relied on several mediating agents who helped identify and contact the respondents. The agents included: the owner of a money transfer shop; the Head of a social cooperative providing welfare and educational services to Extra European migrants; members of local associations involved in activities of cooperation between migrant communities and local citizens; an employee from the Confederation of Crafts and Small and Medium-sized Enterprises. Relying on these intermediaries helped ensure that the inclusion criteria of the sample were respected: the identification of potential candidates was decided by the mediating agents following phone conversations and in-person visits, during which I could discuss the requirements of my study. Moreover, mediating agents had good bonds with the interviewees. Interceding on my behalf, they extensively contributed to creating a comfortable environment for a discussion touching sensitive topics such as money transfers.

Overall, I conducted interviews with 26 migrants. 21 interviews were considered for analysis, while other 5 were excluded because respondents were not meeting the inclusion criteria: 2 moved outside Italy during 2020 just before the enforcement of the national lockdown; other 3 stated that they do not usually send remittances home, either before and after the beginning of the pandemic. Although representing a “small-n“study, interviews were held in a case study logic, whereby each subsequent case provided a more precise knowledge of the issue at hand (Small, 2009).

Interviews were based upon a constructivist approach, adopting a view from below and shedding light on how the experience of sending remittances during the COVID-19 pandemic was subject to local and individual-specific variables (Sumner & Tribe, 2008). The questions asked related to four areas of analysis: migrants’ own experiences with sending remittances home before 2020, to gather insights on how and why they usually remit; migrants’ experiences during the COVID-19 crisis in Italy, the new challenges arisen and their coping strategies; the experience of migrants’ families in their countries of origin; migrants’ remittance behaviour during 2020, whether this has changed due to the pandemic and the factors shaping it.

Field notes were taken during all the interviews and the great majority were audio-recorded and manually transcribed. Transcripts and notes were then processed through thematic analysis, allowing for the organisation of information into emerging themes to uncover the narrative within the data (Skovdal & Cornish, 2015). The coding strategy relied on the combination of deductive and inductive coding. For its deductive part, codes were based on elements pinpointed by studies on resilient remittance flows during 2020, in an attempt to harmonise the findings with the overarching research goals (Saldaña, 2015). For its inductive part, codes highlighted recurrent issues in the interviews (Attride-Stirling, 2001) linked to individual reasons to remit as well as the new and old challenges of sending money home.

DV410 23759

At the beginning of each interview, an information sheet was provided to the respondents and read with them. Participants’ identity was fully anonymised and conditions of confidentiality protected their data. Written consent was asked for every interview except one, for which verbal consent was asked.

Although this approach allows for the collection of more rich and detailed data about personal experiences amid the COVID-19 pandemic, it has several limitations. First, generalisable findings cannot be claimed. The research shows instead that everyone’s personal experience is shaped by multiple factors affecting the respondents, their families in their countries of origin and the modes of remitting. Another limitation of this strategy relates to the sample identification: those who declared themselves available to interview might be inherently different from others rejecting my mediating agents’ request to join the study. Reliance on mainly formal remittance channels and their legal status might place their experience in stark contrast with those of migrants of unclear status. Notwithstanding, this research is highly informative to generate new insights on migrants’ views and perspectives in an understudied setting.

5. Findings

The final sample considered for analysis includes 21 workers of foreign origin coming from European countries (Albania and Romania), Western Africa (Nigeria and Guinea), South Asia (Pakistan) and Northern Africa (Morocco), reflecting the distribution of the most relevant minorities living in the Province of Pistoia. 9 respondents were women, representing the majority of respondents of European origin, while 12 were males and constituted the majority of the Extra-European respondents. The median age of the sample was 31, with European migrants being generally older than Extra-Europeans. Most of the interviewees said to have completed secondary education (13), compared to a minority reporting to have either started or completed one University degree. As per inclusion criteria, all migrants have experience with sending money to their countries of origin. When asked general questions on remitting habits before the pandemic, 15 respondents said to send remittances to their countries of origin regularly . Other 6 claimed to send money irregularly and depending on idiosyncratic needs in their families.

DV410 23759

The sample presents interesting variations regarding the interviewees’ family structure and employment opportunities. 7 respondents said to be living with their families in Italy, while the other 14 live alone and their families still reside in their country of origin. In addition, there are several differences in the occupation of the interviewees, ranging from being employed in construction, manufacturing, personal care, food retail, farming and the nursery sector (the latter being particularly developed in the Province of Pistoia). This variation in occupation and employment status holds important consequences for interviewees’ personal experiences during the pandemic. Out of the sample, 10 respondents claimed that they did not work or worked less during 2020, while the other 11 maintained stable employment. The difference depended on whether they were considered “essential workers“during the several lockdowns implemented in the country, but also on the overall performance of their firms: 4 “essential workers“still witnessed a disruption in their employment, due to limited profits of their businesses.

Turning to the assessment of remittances flows in 2020, migrants’ experiences are stunning proof of resilience. Once asked to compare their experiences with sending money home before and after the COVID-19 outbreak, the analysis confirms that the majority maintained stable remittances towards their home countries. Out of the 21 respondents, only 4 claimed to have sent less money in 2020 compared to the previous years. 8 respondents declared to send more compared to the past, while the other 9 said to have sent as much as before. Remarkably, respondents who reported resilient remittances are a very heterogeneous group based on their origin, family composition, and employment status. First data analysis shows that there is no unambiguous relation between resilient flows and maintaining stable employment throughout the pandemic since many of those reporting stable transactions also declared to have worked less than before.

Similarly, despite constrained resources, migrants sent remittances to their country of origin even when they had to provide for their kids and partners living in Italy The questions of how and why remittance flows could be sustained can only be answered considering each respondent’s individual experience, shaped by a combination of multiple factors. More specifically, interviews show that three elements defined migrants’ experiences with sending steady remittances in 2020. First, migrants’ discourses deeply centred around the new challenges posed by COVID-19 on the livelihoods of their relatives back home, and how these were a major driver of the decision to remit. Second, COVID-19 impact on migrants’ working life in Italy highly constrained their ability to send money, forcing them to implement stressful coping strategies or rely on the support of their social networks. Third, whether the modalities to send remittances changed or remained constant can help explain greater fluxes., The next sections outline the main findings emerging from the thematic analysis with regard to the three areas of analysis. Overall, the findings show that individual experiences should be discussed in light of the factors affecting the demand for remittances, and those involving the supply.

DV410 23759

5.1 A commitment to the family: higher demand for remittances

In line with the literature on altruistic motives behind remittances, commitment towards the family emerged as a dominant theme within the interviews. Sustaining retiree parents, young siblings, partners and children, friends or neighbours was felt as a primary responsibility by the majority of the respondents. For some of them, remittances constitute the family’s single source of income, and “if [migrants] don’t send money, they don’t have anything to eat“(P4). For others, remittances must be regular to support investments in education and cover school fees for younger brothers and children, or to pay rents for the family living back home (P10, P11, P21). Thus, these migrants generally send off a given percentage of their monthly wage. Other 5 respondents claimed to send money irregularly, depending on families’ multifaceted needs, potentially leading to fluctuations in demand for support (P3, P7, P8, P9 & P19). Respondents who do not send remittances regularly still show awareness that they must be ready to send remittances whenever their family asked:

“If something wrong happens to them, I cannot tell them that I do not have money. I must send this money. If they need 40 euros and I only have 20, then I must find a way to earn the other 20 and send 40“(P9).

Notably, the pandemic deteriorated the economic and health conditions of many interviewees’ families, leading respondents to remit more, or more frequently, than before. A remarkable example is offered by Nigerian respondents, who unambiguously pinpointed rampant inflation as a major factor constraining their families’ budget during 2020.Consequently, respondents claimed to send more money back home than before (P6, P10, P11). The nation-wide lockdowns halting normal economic activities (P7), combined with the Nigerian government’s inability to offer support and emergency income to the 220 million Nigerians stranded at home (P2), resulted in increased difficulties purchasing essential goods following the lockdown, which migrants tried to mitigate by sendinggreater amounts (P7). Recurrent lockdowns in the countries of origin were not only forcing migrants to higher transactions, but also unpredicted ones:

DV410 23759

“[P6’s mom] was telling me “Oh, next week there is going to be a lockdown in Nigeria, nobody will go out” so she had to do food shopping that week. It was a rush, and I was like – okay, let me see what I can do, and I was sending money so that she could buy things and take them in the house. […] When she called, I just had to listen to what she said. I had to make sure to give her what she wanted” (P6)

While increased prices during the pandemic were also pinpointed by European respondents (P8, P11,P12, P3, P14), they further referred to a pandemic-driven “reality of precariousness” (P8), leading Romanian and Albanian respondents to send money to young relatives who had recently lost their jobs. A respondent flagged that her son lost his job during the pandemic as the main reason why she sent more remittances in 2020 vis-à-vis previous years (P15).

On top of these economic challenges, European and Extra-European respondents alike showed awareness of the limits of the healthcare systems in their countries of origin, defined as “not very developed” (P18) but also incredibly expensive and profoundly unequal. Talking about Albania, P1 claimed that

“Here, when you go to the hospital, the government covers parts of the expenditures. There, […] you are obliged to pay if you go to the hospital. That’s why we feel obliged to send money, especially for my grandma, because she is old and has health problems”

P2, P3 and P9 said to send money in 2020 to support their parents who had to deal with expensive (but COVID-unrelated) hospitalisations and surgeries, given that Nigerian healthcare is greatly privatised. When I inquired about the functioning of the system, P9 sighed

“Oh, God. If you hurt yourself and you need to visit the hospital, you must pay a deposit. Without a deposit, the doctors do not operate. […] That’s why I sent money. Not only me, but also my other brothers and the sister of my mom contributed to the intervention. The entire family did its best in collecting money”.

While these endemic problems existed well before the pandemic, the latter brought about additional service withdraw and patients’ filtering based on their ability to pay during the pandemic (David Williams et al., 2021). P19 reported that, when her father got COVID-19 at the beginning of 2021, the entire family decided against bringing him to the local hospital. Instead, they opted for curing him at home at their expense, hiring doctors and nurses to reach the house with needed equipment. To finance this safer treatment, P19 sent remittances multiple times throughout the year.

DV410 23759

5.2 Sustaining remittance supply

5.2.1 Migrants’ employment status and government support

Once faced with increased demand from their families, employment status was a major factor shaping migrants’ ability to remit. In this regard, it is informative to compare the experience of interviewees maintaining stable employment during the pandemic vis-à-vis those working less. Remarkably, the latter highlighted the inadequacy and factual limitations of the support measures devised by the Italian government. Although none of the respondents lost their job during the pandemic because of the “Cura Italia” Decree halting lay-offs, those entitled to the CIG said that the support was just insufficient (P9, P21) or poorly delivered (P18, P19). P19 claimed that her husband (the only breadwinner in the family) could not work for nearly three months, but received a small transfer only during the first month. P18 mentioned that the CIG was delivered several months late:

“We didn’t work in March, April, and May. That money was supposed to come at the end of May, but it arrived in October. For three months, we didn’t have anything, we only had the amount of money we kept for ourselves from before”.

Independent workers also declared insufficient or ambiguous support. P4, owning a business not included in the “essential services” typology, claimed that Italian authorities “said they would have helped the businesses and even took our documents to the city hall, but they did not give a cent to anyone”. Instead of helping, they sent a fine to P4’s employees, who had irregularly moved in Tuscany from another Italian region breaking rules preventing inter regional movements. P1, referring to her family’s farm, claimed that they constantly worked throughout the first national lockdown and got support from the government once every two months. However, at the end of the year, they were suddenly asked to pay taxes that were previously exempted. As a consequence of the taxes, they could send fewer remittances in 2021. Other respondents were entitled to other forms of emergency support, including the REM (P2, P3, P17) or a “bonus spesa” (P2) entailing a transfer of 200 euros to buy food or medicines.

Overall, those entitled to emergency help from the government –CIG or REM – were 9, while the other 12 respondents were all employed in sectors defined as “essential” amid the lockdowns, and could maintain stable employment. These data reveal a striking pattern concerning remittance flows: the few respondents who claimed to have sent less money home in 2020 vis-à-vis 2019 were all workers entitled to a form of income support, but declaring it insufficient. As an example, P18 claimed that “the cassa integrazione […] came too late to

DV410 23759

support our families” and again that “it was especially the families in Pakistan who suffered a lot”. P2, who used to send 50% of his monthly income to Africa regularly, was unable to work during the national lockdown and summer 2020 and managed to send money only once. P9 and P21, both entitled to CIG, said that “money was not enough” (P9) for their needs, and they could help his family less than before due to the several expenses they had to bear. P4 showed a great sense of frustration:

“I haven’t worked for 3 or 4 months. I haven’t helped my family for 4 or 5 months”, and added, “in my family of origin my parents got sick but I could not help. When they needed me, I did not manage to help them”.

5.2.2 Coping strategies: savings and reduced consumption

Except for the four respondents reporting worse employment conditions and sending fewer remittances home, the great majority of the migrants sent stable or greater transactions in the face of increased pressures coming from their families. But how could they bear these transfers despite unchanged or worse economic conditions? The answer lies in personal savings and reduced consumption strategies.

Several respondents claimed to have accumulated personal savings before the outbreak of the pandemic (P4, P7, P16, P17, P18, P19). This evidence aligns with data from the National Observatory of Migrant Financial Inclusion, showing that foreign-origin households residing in Italy are progressively revealing a pattern of savings accumulation and protection (Frigeri, 2020b). These savings were important to sustain remittances in the case of P7& P19 or to create some “some deposit” (P16) for greater transfers. P21 also stressed to have used his savings to “make an extra effort” towards his family, although claiming to send less. Others mentioned saving more during the pandemic. This was mostly due to forced national and local lockdowns, reducing consumption possibilities, and discouraging the utilisation of services (Immordino et al., 2021; Ercolani et al., 2021). Increased savings then reflect in higher remittances. For example, P11, working as a full-time caregiver, said that she once transferred her entire monthly wage to her daughter’s bank account in Romania, because she was not undergoing any expense during the national lockdown. P14 also mentioned working overtime and bearing little expenses during the local lockdowns of Q4 2020 and Q1 2021, allowing her to send more.

DV410 23759

Together with reliance on savings, cutting expenditures was a first-order strategy to endure higher remittances. Several conversations revealed this.

“I was able to send more because there was less left for me. I go to the same job, but now I minimise my spending. I stopped going to restaurants, to retail, I stopped going to many places. I just stayed home to cut the expenses short” (P10)

Or

“I saved on little things, for example, I didn’t do food shopping like before. I also saved because I didn’t spend on things I really needed” (P4).

Additionally, P17 said that he could send money home during the pandemic because he shares his accommodation with seven other workers, thus bearing meagre expenses.

Remarkably, these coping strategies caused great distress to the respondents, especially those living with their families in Italy while economically supporting other relatives or friends in their countries of origin.

“The situation was so critical also for me by then. It was very difficult for me to take care of myself here and send money to my family” (P7).

Similarly, P6 claimed that providing for his families in Italy and abroad really “affected [him] financially”, because “what you saved before, you are going to take it” (and spend it). P19 claimed that accumulating money for her parents abroad “was not easy” with only one person working in the household and that they “put a big effort” to ensure transactions. P10, who was unable to work during 2020 and received an extremely delayed CIG, claimed

“It is difficult to manage because, of course, I am not rich. I can’t just keep giving, otherwise, I will remain with zero for myself”.

5.2.3 Coping strategies: reliance on social networks

Albeit overlooked by the nascent literature on resilient remittance flows during 2020, a recurrent theme across the interviews regarded the role played by social networks in sustaining remittance flows before and throughout the pandemic. Together with trust and shared norms, social networks are a defining element of social capital, which facilitates coordinated actions and allows for accomplishing goals that would otherwise be impossible to achieve (Putnam, 1993).

DV410 23759

Out of the interview sample, 7 respondents declared to participate in at least one institutionalised community-level group, including local associations or religious communities. Additionally, 3 respondents referred to strong bonds existing within intra-ethnic groups, also covering a role of importance in sustaining the livelihoods of migrant workers.

Interviews outcomes show that local associations played an important role in collecting and deploying resources to support both local members and relatives living abroad during the pandemic. P1 and P8 mentioned that their local association actively sustained needy households back in their home country.

“if someone in the association knew families in need, they talked with the rest of the group and the members were getting together to send money there. This money was sent not only to people in need in Albania but also in Pistoia”. (P8)

Moreover, social networks proved fundamental in overcoming the practical difficulties of the national lockdown lasting from March to May 2020. P11, P12 & P13 depicted a situation of great distress for the foreign-born caregiver population. They referred to some caregivers who were “buried alive for four months” within the houses of the elderly people they worked with, because their employers put pressure on them never to leave the house (P15). As a result, caregivers who regularly went to MTO shops could not physically reach these venues. In such a scenario, carers who could leave home took responsibility for making transactions on their friends’ behalf.

“When I couldn’t leave the house, I was calling A. and asking her “A., please, send for me 300 euros”. And then, when we were meeting again, I was giving money back to her”. (P11)

“We were helping each other. Once one was going to the shop, she was sending money for all”. (P12)

Reciprocal help was also a means to overcome other types of challenges. For example, P8 claimed that she often made transactions via Western Union on behalf of younger and inexperienced co-workers in her firm. Similarly, P4 reported that, before the pandemic, he supported his employees by making transactions on their behalf. P12 mentioned that remittance senders might overcome the weekly transfer amount allowed by MTOs (around 1000 euros). In these cases, asking friends to send money on one’s behalf is a common coping strategy.

DV410 23759

Finally, even in the absence of formal associations, social networks provide a quick form of lending at zero interest (P8). P4, who was unable to send remittances between May and July 2020, claimed to have exceptionally borrowed money from his friends to support his family during the Muslim festival of Id al-Adha in July 2020.

5.3 Remittances channels

Interviewees reported heterogeneous experiences regarding their main remittance channel used. While Extra-European migrants mostly rely on MTOs accessible either through online applications or brick-and-mortar shops, European migrants adopt a wider range of formal and informal modes, confirming that lower distance and negligible travel costs enhance informality (Ferriani and Oddo, 2019). Their remittance modes include bank transfers and MTOs, as well as the physical transport of cash across national borders and sending packages containing goods and cash.

It is worth pointing out that these flows are unrecorded but legal: migrants can freely cross national borders carrying cash until 10,000€, beyond which a declaration is required (P21). As P8 put down, “the people I know don’t do weird things”, meaning that they just carry small amounts with them every time they come home.

Respondents showed great awareness of the relative perks of different remittance modes. They generally describe MTOs such as Western Union as faster and cheaper (P2, P3, P11, P12, P13, P19). Instead, there are mixed feelings towards transactions made through banks transfers and post offices, which are said to be slower in executing transactions (P4, P12) but also ask for personal details and are more expensive (P4, P5, P21). Migrants also compare exchange rates when opting for one MTOs rather than another (P10).

Among the others, trust was a major variable driving preference between digital or cash remittances, as well as formal versus informal channels. Among Extra-European migrants, physically going to a shop offering money transfer services is preferred to using apps, because it allows migrants to “make sure of what [the operators] do” (P9) and receive face-to-face support during the transactions (P6, P16). Digital remittances are preferred by respondents who are more familiar with technological devices, but also those with tight working schedules and who cannot reach money transfer shops, which are located in the main urban areas of the Province of Pistoia but not in the smaller municipalities (P6, P17, P18). Moreover, P17 and P18 mentioned being particularly at ease using an app fully operating and providing assistance in Urdu – their native language- while knowing that the app was legal. Noting that “In Pakistan, the biggest source of foreign currency is overseas Pakistani”, P18 claimed that “sending by a proper channel or a proper system, is good for the country”.

DV410 23759

Lack of trust towards agents and institutions, as well as avoidance of transaction fees, provides a rationale for the prevalence of cash hand-carrying among Albanian respondents.

“People are scared that, maybe, if they send too much money, someone can come and bother them. I have spoken with my friends, and they said they don’t want to be accountable to anyone. If they want to send 100 euros more to Albania, they don’t want anyone to come and ask them if there’s a reason for that. They trust themselves more than going to Western Union and having to justify their choices” (P8).

Overall, respondents did not seem to have changed their preferred remittance channels during the pandemic. Those relying on money transfer shops did not encounter greater difficulties in accessing physical services, coherently with the evidence that tobacco shops, post offices and money transfer shops kept operating amid national and local lockdowns. Two remarkable exceptions are P6 and P14, who used to travel across different municipalities within the province to reach cheaper money transfer shops. As crossing municipal borders was strictly forbidden during the lockdowns, P6 relied on digital payments through online applications and P14 sent money from closer but more expensive money transfer venues.

Finally, the experience of European and Northern African migrants provides relevant insights that complement recent evidence of a COVID-led formalisation of remittance flows (Dinarte et al., 2021). Within my sample, only two respondents said to have relied more on formal fluxes compared to the past. P8 pointed that she transferred money with MTOs when she could not go to Albania during 2020. P19 also relied on Western Union because she needed “the fastest way to transfer money” and could not wait to travel to Albania or entrust money to travelling relatives. On the other hand, there is evidence that informal channels persisted during the pandemic, mainly through parcels and packages. These packages are generally entrusted to lorry drivers who frequently make the route between Italy and migrants’ country of origin. European caregivers pinpointed reliance on such a system

“These lads come to your house, collect packages and bring them to Romania. […] They can cross regional borders because they declare everything to the customs, otherwise they get everything confiscated. Then, our families back home have an address where they can go, for example, a supermarket, and all the people gather in front of the supermarket. The lads have a list in their phone with all the names of the people who have to withdraw money” (P11)

DV410 23759

P21, talking about an acquaintance working as a lorry driver, said that they could work during the lockdown as essential workers, and delivered money on behalf of their clients. She also pointed out that such a system is deeply trusted, and thrived during the pandemic.

5.4 Discussion

The diversity of experiences reported in the interviews augments the existing literature on resilient flows in 2020 by providing relevant insights.

First, migrants’ discourses demonstrate that sending money home in times of crisis is a complex decision. It is shaped by multiple factors linked to the demand for remittances coming from their families, as well as the supply of remittances hinging on COVID-19 impact in Italy. In line with altruism and insurance motives theories, interviews show that steady or higher transactions were sent to provide a lifeline for their families and communities despite novel pandemic-driven economic and health challenges, driving up the demand for remittances. Once faced with higher or unchanged demand and unmuted or worsened economic conditions, migrants implemented a set of stressful coping strategies, including reliance on savings and reduced consumption. Some of them also requested support from their social networks.

Thus, a unifying framework to interpret migrants’ experience should concomitantly assess variables affecting demand and supply, including access to savings systems and strength of social ties, rather than focusing on the macro-level variables discussed by the WB (2021a). Second, the findings invite caution when assessing the perks of government intervention in sustaining higher remittance flows. Migrants not employed in “essential sectors” and those experiencing lower employment were all entitled to emergency support from the Italian government.However, government support proved insufficient to send money home, confirming evidence that fiscal stimulus packages did not effectively contribute to sustaining livelihoods in the Italian case (Dinerte et al., 2021; Capps et al., 2020; OECD 2020a). On the contrary, those employed in “essential sectors” could regularly work during the lockdowns hampering economic activities in Italy, and were able to endure steady remittances by implementing several coping strategies. The fact that most of the migrants in my sample were employed in essential sectors reveals another consequence of the COVID-19 pandemic: uncovering the importance of migrant labour in crucial sectors for the survival of Italian society (ISMU, 2021).

DV410 23759

Third, the research has shown several practices and widespread beliefs regarding the use of different remittance channels. Because most of the respondents highly value reaching money transfer shops and relying on in-person support, the early decision to keep RSPs open greatly enhanced remittance flows in the Italian case (Frigeri, 2020b). Moreover, this study offers limited evidence on the occurred shift from informal to formal channels claimed by the literature (Ratha et al., 2021; RCT, 2020). First, the majority of the European and Northern African respondents reported utilising formal remittance channels much more than informal ones, even before thepandemic’s beginning . Second, interviewees claimed that informal systems persisted during the pandemic. In this regard, further research focused on European migrants is needed to uncover more evidence.

6. Conclusion

This thesis sought to explore the experiences of migrants living in Italy and sustaining resilient remittance flows amid the COVID-19 pandemic. By relying on semi-structured in-depth interviews with 21 foreign workers in the Province of Pistoia (Tuscany), it aimed to contribute to a nascent literature thread looking into the factors explaining steady international remittances in 2020.

It revealed that the great majority of interviewees sent regular or higher remittances home during 2020. This resulted from increased demand for economic support from families based in the countries of origin, who experienced relevant health and economic challenges. To fulfil their family’s commitment despite unchanged or worsened economic conditions, migrants undertook a set of coping strategies including reliance on their savings, reducing consumption, or relying on social networks. Migrants reporting lower remittances experienced a significant worsening of their economic conditions and received scant and insufficient emergency support.

Most migrants relied on the same RSPs they used before the pandemic. A minority relied more on formal systems compared to before, while others reported the coexistence of formal and informal channels. Overall, the study confirms that remittances are a stable, countercyclical income flux on which households abroad can extensively rely in moments of global crisis. Additionally, it endorses a framework to understand migrants’ experiences by analysing how the pandemic impacted remittance-recipient families, driving up thedemand for money , and remittance-senders, constraining the supply. Although this exploratory research focuses on Italy and its data was collected in a medium-size province, the lessons shared by the respondents and the framework to interpret them can be applied to different migrant communities and countries to augment research on resilient remittances.

DV410 23759

Bibliography

Acosta, P.A., Baez, J., Beazley, R and Murruga, E., (2012), “The Impact of the Financial Crisis on Remittance Flows: The Case of El Salvador”, Migration and Remittances during the Global Financial Crisis and Beyond, 183-191.

Adams Jr, R. H., & Cuecuecha, A. (2013). The impact of remittances on investment and poverty in Ghana. World Development, 50, 24-40.

Attride-Stirling, J. (2001). Thematic networks: an analytic tool for qualitative research. Qualitative research, 1(3), 385-405.

Balch, O. (2020). Are digital payments COVID winners? Raconteur, 10 May 2020. (also available at raconteur.net/finance/digital-payments-covid-19) Bank of Italy. (2021).

Foreign workers’ Remittances. [Data file]. Retrieved from: https://www.bancaditalia.it/statistiche/tematiche/rapporti-estero/rimesse-immigrati/

Barajas, A., Chami, R., Fullenkamp, C., & Garg, A., (2010), “The Global Financial Crisis and Workers’ Remittances to Africa: What’s the Damage?”, In IMF Working Papers (WP/10/24; IMF Working Papers, Issue WP/10/24).

Benni, N. (2021). Digital finance and inclusion in the time of COVID-19: Lessons, experiences and proposals. Rome, FAO.

Beuermann, D.W., Ruprah, I.J. & Sierra, R.E. (2016). Do remittances help smooth consumption during health shocks? Evidence from Jamaica. The Journal of Developing Areas, 50 (3), pp. 1-19.

Capps, R., Batalova, J., & Gelatt, J. (2020). COVID-19 and Unemployment: Assessing the Early Fallout for Immigrants and Other US Workers. Migration Policy Institute.

Chami, R., Fullenkamp, C., & Jahjah, S. (2005). Are immigrant remittance flows a source of capital for development?. IMF Staff papers, 52(1), 55-81.

Conteduca, F.P. (2021). Measuring covid-19 restrictions in Italy during the second wave. Bank of Italy, Mimeo

Cox, E., & Ureta, M., (2003). International migration, remittances, and schooling: Evidence from El Salvador. Journal of Development Economics, 72(2), pp. 429–461.

DV410 23759

David Williams, O., Yung, K. C., & Grépin, K. A. (2021). The failure of private health services: COVID-19 induced crises in low-and middle-income country (LMIC) health systems. Global Public Health, 1-14.

Delle-Monache, D., Emiliozzi, S., & Nobili, A. (2021). Tracking economic growth during the Covid-19: a weekly indicator for Italy. Bank of Italy, Mimeo.

Diaz, V., and Soydemir, G., (2013). “Regional foreclosures and Mexican remittances: Evidence from the housing market crisis”, North American Journal of Economics and Finance, 24, 74–86.

Dinarte, L., Jaume, D., Medina-Cortina, E., & Winkler, H. (2021). Neither by Land nor by Sea: The Rise of Electronic Remittances during COVID-19.

Docquier, F., Rapoport, H., & Salomone, S. (2012). Remittances, ’migrants’ education and immigration policy: Theory and evidence from bilateral data. Regional Science and Urban Economics, 42(5), 817-828.

Ercolani, V., Guglielminetti, E., & Rondinelli, C. (2021). Fears For The Future: Saving Dynamics After The Covid-19 Outbreak. Covid-19 note, Bank of Italy, forthcoming.

European Migration Network, Organisation for Economic Cooperation and Development. (2020). Impact of Covid-19 on remittances in EU and OECD countries: EMN and OECD Inform #4.

Retrieved Eurostat. (2021). Population on 1 January by age, sex and broad group of citizenship. [Data

file]. from: /MIGR_POP2CTZ https://ec.europa.eu/eurostat/en/web/products-datasets/

Fasani F., & Mazza J. (2020), Immigrant Key Workers: Their Contribution to Europe’s COVID-19 Response.

Ferriani, F., & Oddo, G. (2019). More distance, more remittance? Remitting behavior, travel cost, and the size of the informal channel. Economic Notes: Review of Banking, Finance and Monetary Economics, 48(3), e12146.

Frankel, J., (2011). Are bilateral remittances countercyclical? Open Economies Rev 22, 1–16.

Frigeri, D. (2020a). Le rimesse dei migranti e il COVID-19. Il caso italiano, un esempio diresilienza? Centro Studi di Politica Internazionale

DV410 23759

Frigeri, D. (2020b). Oltre la bancarizzazione, il volano risparmio-credito e investimenti. Dossier Statistico Immigrazione, Idos

GSMA, (2021). State of the Industry Report on Mobile Money. GSMA Mobile Money Programme.

Gubert, F. (2002). Do Migrants Insure Those who Stay Behind? Evidence from the Kayes Area (Western Mali). Oxford Development Studies, 30(3), pp.267–287.

Gupta, P. (2006). Macroeconomic determinants of remittances: evidence from India. Economic and Political Weekly, 2769-2775.

Gyimah-Brempong, K., & Asiedu, E. (2015). Remittances and investment in education: Evidence from Ghana. The journal of international trade & economic development, 24(2), 173-200.

Hanson, G., & Woodruff, C., (2003). Emigration and educational attainment in Mexico. Mimeo, San Diego: University of California.

Holtzblatt, J., Karpman, M., 2020. Who Did Not Get the Economic Impact Payments by Mid to-Late May, and Why? Technical Report. Urban Institute

IMF (2020). Regional Economic Outlook for the Middle East and Central Asia. Washington, DC.

IMF (2021a). Fiscal Monitor: A fair Shot. Washington, April

IMF (2021b), Fiscal Monitor Database of Country Fiscal Measures in Response to the COVID 19 pandemic, accessed via https://www.imf.org/en/Topics/imf-and-covid19/Fiscal Policies-Database-in-Response-to-COVID-19

Immordino, G., Jappelli, T., Oliviero, T., & Zazzaro, A. (2021). Fear of COVID-19 Contagion and Consumption: Evidence from a Survey of Italian Households. CSEF, Centre for Studies in Economics and Finance, Department of Economics, University of Naples.

ISMU (2021). The Twenty-sixth Italian Report on Migrations 2020.

ISTAT (2021a). Yearly data on Foreign Residents by Province and Citizenship. [Data file]. Retrieved from: http://dati.istat.it/

ISTAT (2021b). Gross Domestic Product (expressed in seasonally and calendar adjusted chain linked values; reference year 2015). [Data file]. Retrieved from: http://dati.istat.it/

DV410 23759

ISTAT (2021c). Quarterly data on Unemployment Rates for Foreign Residents and Italians. [Data file]. Retrieved from: http://dati.istat.it/)

Leonardi, R., Nanetti, R. Y., & Putnam, R. D. (2001). Making democracy work: Civic traditions in modern Italy. Princeton, NJ: Princeton university press.

Lucas, R., & Stark, O., (1985). Motivations to Remit: Evidence from Botswana. Journal of Political Economy, 93(5), pp.901–918.

Lueth, E., & Ruiz-Arranz, M., (2008). Determinants of bilateral remittance flows. BEJM 8

Mahoney, J., & Goertz, G. (2006). A tale of two cultures: Contrasting quantitative and

qualitative research. Political Analysis, 14(3), 227–249

Mason, J. (2002). Qualitative researching (2nd ed.). London; Thousand Oaks, Calif.: Sage Publications.

OECD. (2020a). What is the Impact of the COVID-19 Pandemic on Immigrants and Their Children?. OECD Publishing.

OECD. (2020b). The Impact of the coronavirus (COVID-19) crisis on development finance. OECD Publishing.

OECD. (2021a). Foreign population (indicator). [Data file]. Retrieved from: https://data.oecd.org/migration/foreign-population.htm#indicator-chart

OECD. (2021b). Quarterly GDP (indicator). [Data file]. Retrieved from:

https://data.oecd.org/gdp/quarterly-gdp.htm

Orozco, M., & Klaas, K. (2021). A commitment to Family: Remittances and the COVID-19

Pandemic – Experiences of US migrants. Inter-American Dialogue. Washington DC.

Osili, U. O. (2004). Migrants and housing investments: Theory and evidence from Nigeria. Economic development and cultural change, 52(4), 821-849.

Raihan, S. (2010). Impact of the Global Financial Crisis on Migration and Remittances in Bangladesh: A Survey Based Analysis. MPRA Paper No. 37946

Rapoport, H., & Docquier, F. (2006). The economics of ’migrants’ remittances. Handbook of the economics of giving, altruism and reciprocity, 2, 1135-1198.

Ratha, D. (2017). What are Remittances? Finance & Development, IMF.

DV410 23759

Ratha, D., De, S., Kim, E. J., Plaza, S., Seshan, G. K., & Yameogo, N. D. (2021). Resilience: COVID-19 crisis through a migration lens. Migration and Development Brief, 34.

Ratha, D., De, S., Kim, E. J., Plaza, S., Seshan, G. K., & Yameogo, N. D. (2020). COVID-19 crisis through a migration lens. Migration and Development Brief, 32.

Remittance Community Task Force (RCTF) (2020). Remittances in crisis: Response, Resilience, Recovery. International Fund for Agricultural Development

Ruiz, I., & Vargas-Silva, C. (2010). Another consequence of the economic crisis: a decrease in migrants’ remittances. Applied Financial Economics, 20(1-2), 171-182.

Saldaña, J. (2021). The coding manual for qualitative researchers. Sage.

Sanchez, D. G., Parra, N. G., Ozden, C., & Rijkers, B. (2020). Which jobs are most vulnerable to COVID-19? What an analysis of the European Union reveals. World Bank Research and Policy Briefs.

Sidaoui, J., Ramos-Francia, M., & Cuadra, G. (2010). The global financial crisis and policy response in Mexico. BIS papers, (54), 279-298.

Sirkeci, I., Cohen, J. H., & Ratha, D. (Eds.). (2012). Migration and remittances during the global financial crisis and beyond. World Bank Publications.

Skovdal, M., & Cornish, F. (2015). Qualitative research for development: a guide for practitioners. Rugby: Practical Action Publishing.

Small, M. L. (2009). How many cases do I need? On science and the logic of case selection in field-based research. Ethnography, 10(1), 5-38.

Stark, O. (2009). Reasons for remitting. ZEF discussion papers on development policy, (134).

Sumner, A., & Tribe, M. A. (2008). International development studies: Theories and methods

in research and practice. Sage.